- Nonfarm Payrolls (PAYEMS): +336k (+2.03%) m/m.

- Auto/Light Truck Sales (ALTSALES): 323k (+2.06%) m/m.

- Durable Goods Orders (DGORDER) 284B (+420M +2.06%) m/m.

- 30 Year Mortgage (MORTGAGE30US): 7.49% (+18 bp); new high.

- 10 Year Treasury (DGS10): 4.79% (+20 bp); new high.

- Fed Balance Sheet (WALCL): -46B (-0.58%) w/w.

- Total Bank Credit (TOTBKCR): -5.9B (-0.03%) w/w.

- Strategic Petroleum Reserve (WCSSTUS1): +300k (+0.09%) w/w; slight refill.

Payrolls were surprisingly strong (expected 160k, actual 336k), and this drove some pretty impressive market volatility on Friday – first a plunge in gold silver, equities, and the Euro, followed by an even stronger bounce-back rally – 30 minutes later in the metals, and about 2 hours later in equities and the Euro. I don’t pretend to understand why these violent moves happened – first in one direction, then the other. To me, it seems as though “higher for longer” remains in place – CME Fedwatch says 27% chance of a rate hike at the meeting on November 1, with no chance of a rate cut.

While “20 basis points” doesn’t look like a very big move in the 10-year yield (red line), it translated into a 4.4% drop in the value of the 20-year bond fund TLT this week alone, and a 50% loss to capital (candlesticks) for anyone who bought this fund back in mid-2020 at $171/share. Big buyers of bonds are pension funds, and banks. The new high in the 10-year yield was the big news for the week, at least for me anyway. Note that the 30-year mortgage rate is closely tied (directionally) to the 10-year yield; both yields hit new highs this week.

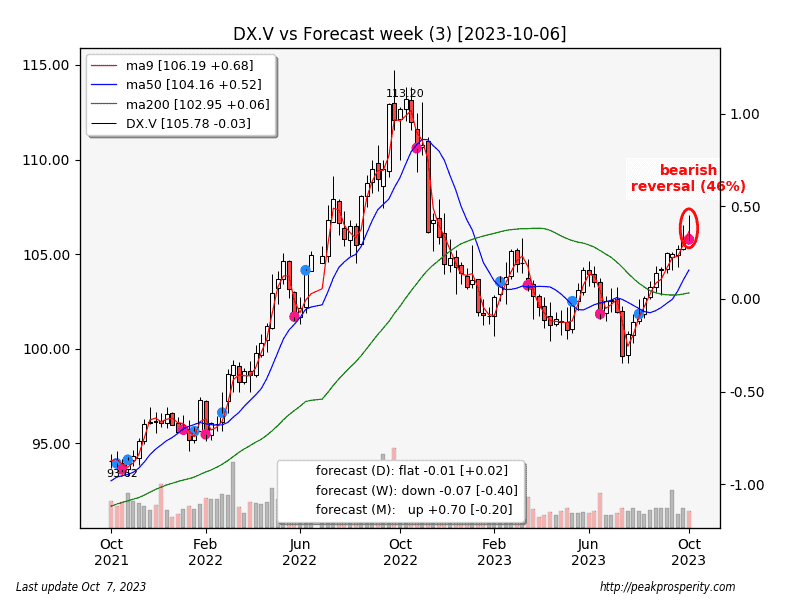

The buck broke out to a new 10-month high (almost 1.07) early in the week, but then sold off fairly hard on Thursday and Friday, erasing the gains and printing a bearish-looking “northern doji” candle with that disagreeable long upper shadow. This was enough to flip my trend model into a shallow downtrend. Why did this reversal happen? No idea – the Euro had a similar move, in reverse, but it remains in a downtrend. We’ll have to see if the dollar top gets confirmed next week with a lower close.

How is the dollar-to-confetti operation going? Confetti moved higher this week, with RMB(/USD)

by davefairtex

by davefairtex