Chris Martenson

As bad as the US is, there are worse problems elsewhere. This is why I think this credit crisis will not play out like any previously and why I think there’s a better than even chance of a systemic banking crisis.

In times past when a country experienced a bubble or a banking crisis, there was always a country next door that hadn’t where the savvy could hide out. Where does one hide out today?

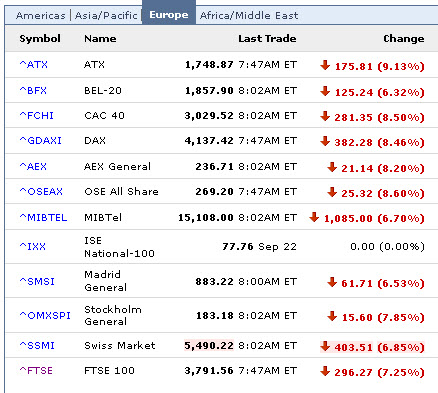

Europe on the brink of currency crisis meltdown

The financial crisis spreading like wildfire across the former Soviet bloc threatens to set off a second and more dangerous banking crisis in Western Europe, tipping the whole Continent into a fully-fledged economic slump.Currency pegs are being tested to destruction on the fringes of Europe’s monetary union in a traumatic upheaval that recalls the collapse of the Exchange Rate Mechanism in 1992.

“This is the biggest currency crisis the world has ever seen,” said Neil Mellor, a strategist at Bank of New York Mellon.

Stephen Jen, currency chief at Morgan Stanley, says the emerging market crash is a vastly underestimated risk. It threatens to become “the second epicentre of the global financial crisis,” this time unfolding in Europe rather than America.

Austria’s bank exposure to emerging markets is equal to 85pc of GDP – with a heavy concentration in Hungary, Ukraine, and Serbia – all now queuing up (with Belarus) for rescue packages from the International Monetary Fund.

Exposure is 50pc of GDP for Switzerland, 25pc for Sweden, 24pc for the UK, and 23pc for Spain. The US figure is just 4pc. America is the staid old lady in this drama.

Those figures in the bottom two paragraphs are quite the eye-openers. Somehow Austria’s bank system loaned out 85% of Austria’s GDP to emerging markets that are even now resorting to emergency measures to stem the erosion of the their currencies against the dollar. The problem, apparently, is that these countries were loaned vast amounts of money denominated in dollars. The faster their currencies fall, the more it costs them to pay back their loans.

Some of these currencies have fallen by 40% in a matter of weeks.

International instability

As bad as the US is, there are worse problems elsewhere. This is why I think this credit crisis will not play out like any previously and why I think there’s a better than even chance of a systemic banking crisis.

In times past when a country experienced a bubble or a banking crisis, there was always a country next door that hadn’t where the savvy could hide out. Where does one hide out today?

Europe on the brink of currency crisis meltdown

The financial crisis spreading like wildfire across the former Soviet bloc threatens to set off a second and more dangerous banking crisis in Western Europe, tipping the whole Continent into a fully-fledged economic slump.Currency pegs are being tested to destruction on the fringes of Europe’s monetary union in a traumatic upheaval that recalls the collapse of the Exchange Rate Mechanism in 1992.

“This is the biggest currency crisis the world has ever seen,” said Neil Mellor, a strategist at Bank of New York Mellon.

Stephen Jen, currency chief at Morgan Stanley, says the emerging market crash is a vastly underestimated risk. It threatens to become “the second epicentre of the global financial crisis,” this time unfolding in Europe rather than America.

Austria’s bank exposure to emerging markets is equal to 85pc of GDP – with a heavy concentration in Hungary, Ukraine, and Serbia – all now queuing up (with Belarus) for rescue packages from the International Monetary Fund.

Exposure is 50pc of GDP for Switzerland, 25pc for Sweden, 24pc for the UK, and 23pc for Spain. The US figure is just 4pc. America is the staid old lady in this drama.

Those figures in the bottom two paragraphs are quite the eye-openers. Somehow Austria’s bank system loaned out 85% of Austria’s GDP to emerging markets that are even now resorting to emergency measures to stem the erosion of the their currencies against the dollar. The problem, apparently, is that these countries were loaned vast amounts of money denominated in dollars. The faster their currencies fall, the more it costs them to pay back their loans.

Some of these currencies have fallen by 40% in a matter of weeks.

Here are some interesting stories I collected this week.

US surrenders power to appoint World Bank president

The US is to lose its power to appoint the president of the World Bank after the UK’s development secretary, Douglas Alexander, brokered a deal to throw open the post to candidates from any country.Backed by European governments and developing countries, Alexander overcame resistance from the US and Japan to secure a reform he described last night as "a significant step forward".

My Comment: This may not seem like much, but symbolically it is huge. The World Bank wields enormous influence, and for Europe, et al., to demand, and receive, the right to fill the post speaks volumes about US prestige and power at this time.

US losing influence, housing starts, and the next Iceland

Here are some interesting stories I collected this week.

US surrenders power to appoint World Bank president

The US is to lose its power to appoint the president of the World Bank after the UK’s development secretary, Douglas Alexander, brokered a deal to throw open the post to candidates from any country.Backed by European governments and developing countries, Alexander overcame resistance from the US and Japan to secure a reform he described last night as "a significant step forward".

My Comment: This may not seem like much, but symbolically it is huge. The World Bank wields enormous influence, and for Europe, et al., to demand, and receive, the right to fill the post speaks volumes about US prestige and power at this time.

As the US government and Federal Reserve work tirelessly to assure that the engines of a debt-based economy (the banks and lending institutions) remain well-supplied with capital and liquidity, the wheels are falling off.

First, retail sales and store traffic suffered some of the most pronounced drops on record in September, indicating that a consumer-led recession is upon us – which would make this the first one since 1991.

…the number of people in U.S. malls and department stores declined 9.3% year over year in September. The U.S. Commerce Department this morning reported that retail sales fell 1.2% in September, marking the biggest decline in three years.

Next, a measure of manufacturing activity in the Philadelphia and NY regions and a different measure of nationwide manufacturing capacity utilization both took very sharp turns for the worse:

WASHINGTON (MarketWatch) — Turmoil in the credit markets has spilled over with a vengeance into the factory sector in the Philadelphia region, the Philadelphia Federal Reserve said Thursday.

The Philly Fed index plunged to a reading of negative 37.5 in October from a positive 3.8 in September. It was the sharpest one-month decline on record and marked the lowest level for the gauge in 18 years. On Wednesday, the New York Fed reported that factory activity in the Empire State region also fell sharply.In addition, about 43% said the recent turmoil had forced them to scale back their capital-spending plans.

The region’s manufacturing executives expect no growth over the next six months. The index of future activity fell to negative 4.2 from 30.8 in the previous month.

Earlier Thursday, the Federal Reserve reported a stunning 2.6% drop in industrial production in September, the biggest one-month drop in 34 years.

The data "make clear that the factory sector has taken a powerful turn for the worse," Action Economics said in a note to clients. "In total, since August, the economy has shifted from a profile of remarkable resilience to one of freefall at a pace that is consistent with a sizable, rather than mild, recession," Action Economics said.

The real economy – manufacturing and sales are off … way off.

As the US government and Federal Reserve work tirelessly to assure that the engines of a debt-based economy (the banks and lending institutions) remain well-supplied with capital and liquidity, the wheels are falling off.

First, retail sales and store traffic suffered some of the most pronounced drops on record in September, indicating that a consumer-led recession is upon us – which would make this the first one since 1991.

…the number of people in U.S. malls and department stores declined 9.3% year over year in September. The U.S. Commerce Department this morning reported that retail sales fell 1.2% in September, marking the biggest decline in three years.

Next, a measure of manufacturing activity in the Philadelphia and NY regions and a different measure of nationwide manufacturing capacity utilization both took very sharp turns for the worse:

WASHINGTON (MarketWatch) — Turmoil in the credit markets has spilled over with a vengeance into the factory sector in the Philadelphia region, the Philadelphia Federal Reserve said Thursday.

The Philly Fed index plunged to a reading of negative 37.5 in October from a positive 3.8 in September. It was the sharpest one-month decline on record and marked the lowest level for the gauge in 18 years. On Wednesday, the New York Fed reported that factory activity in the Empire State region also fell sharply.In addition, about 43% said the recent turmoil had forced them to scale back their capital-spending plans.

The region’s manufacturing executives expect no growth over the next six months. The index of future activity fell to negative 4.2 from 30.8 in the previous month.

Earlier Thursday, the Federal Reserve reported a stunning 2.6% drop in industrial production in September, the biggest one-month drop in 34 years.

The data "make clear that the factory sector has taken a powerful turn for the worse," Action Economics said in a note to clients. "In total, since August, the economy has shifted from a profile of remarkable resilience to one of freefall at a pace that is consistent with a sizable, rather than mild, recession," Action Economics said.

One of the dominant myths of America is that we practice one of the

freest forms of capitalism on the face of the planet. Hard work and

prudence are rewarded, while Schumpeter’s ‘creative destruction’ quickly cleans out the mistakes.

Unlike most myths, this one apparently lacks a kernel of truth at the core.

As the details emerge over the various bailouts and market distortions,

it is becoming clearer that moral hazard has been increased, not

lessened, and that those who behaved prudently during the credit bubble

insanity are going to be punished.

Some are getting angry:

[quote]Community banking executives around the country responded

with anger yesterday to the Bush administration’s strategy of investing

$250 billion in financial firms, saying they don’t need the money,

resent the intrusion and feel it’s unfair to rescue companies from

their own mistakes.

And in offices around the country, bankers simmered.

Peter Fitzgerald, chairman of Chain Bridge Bank in McLean, said he was "much

chagrined that we will be punished for behaving prudently by now having

to face reckless competitors who all of a sudden are subsidized by the

federal government."

At Evergreen Federal Bank in Grants Pass, Ore., chief executive Brady

Adams said he has more than 2,000 loans outstanding and only three

borrowers behind on payments. "We

don’t need a bailout, and if other banks had run their banks like we

ran our bank, they wouldn’t have needed a bailout, either," Adams said. [/quote]

Punishing the Prudent

One of the dominant myths of America is that we practice one of the

freest forms of capitalism on the face of the planet. Hard work and

prudence are rewarded, while Schumpeter’s ‘creative destruction’ quickly cleans out the mistakes.

Unlike most myths, this one apparently lacks a kernel of truth at the core.

As the details emerge over the various bailouts and market distortions,

it is becoming clearer that moral hazard has been increased, not

lessened, and that those who behaved prudently during the credit bubble

insanity are going to be punished.

Some are getting angry:

[quote]Community banking executives around the country responded

with anger yesterday to the Bush administration’s strategy of investing

$250 billion in financial firms, saying they don’t need the money,

resent the intrusion and feel it’s unfair to rescue companies from

their own mistakes.

And in offices around the country, bankers simmered.

Peter Fitzgerald, chairman of Chain Bridge Bank in McLean, said he was "much

chagrined that we will be punished for behaving prudently by now having

to face reckless competitors who all of a sudden are subsidized by the

federal government."

At Evergreen Federal Bank in Grants Pass, Ore., chief executive Brady

Adams said he has more than 2,000 loans outstanding and only three

borrowers behind on payments. "We

don’t need a bailout, and if other banks had run their banks like we

ran our bank, they wouldn’t have needed a bailout, either," Adams said. [/quote]

Regarding the expansion of the FDIC powers to include guaranteeing the senior debt of banks and their holding companies…in reviewing the details, I think I figured it out.

Here’s the text:

The Secretary of the Treasury, in consultation with the President and upon the recommendation of the Boards of the FDIC and the Federal Reserve, has invoked the systemic risk exception of the FDIC Improvement Act of 1991. [Edit: love the name]

This action will provide the FDIC with flexibility to provide a 100 percent guarantee for newly-issued senior unsecured debt and non-interest bearing transaction deposit accounts at FDIC insured institutions subject to the terms outlined below.

Scope of Eligible Entities

Eligible institutions would include: 1) FDIC-insured depository institutions, 2) U.S. bank holding companies, 3) U.S. financial holding companies, and 4) U.S. savings and loan holding companies that engage only in activities that are permissible for financial holding companies to conduct under section 4(k) of the Bank Holding Company Act ("Eligible Entities").

Not all companies are eligible, but "bank holding companies" are eligible.

Hmmmm…seems that I recently heard something about somebody switching from being an investment bank to a bank holding company recently…who was that? Oh. Here it is.

On Sept. 21, in a move that fundamentally changed the shape of Wall Street, Goldman and Morgan Stanley, the last major American investment banks, asked the Federal Reserve to change their status to bank holding companies.

Goldman would now look much like a commercial bank, with significantly tighter regulations and much closer supervision by bank examiners from several government agencies.

Yes, I remember being confused by this move at the time as it made no sense. At least the explanations did not smell right. We were told that GS and MS "asked" to be placed under "significantly tighter regulations and much closer supervision by bank examiners from several government agencies."

That would have been a first.

It is now clear to me what happened. The government guarantee of all senior debt was already in the works some time ago, and GS and MS hopped on that gravy train. At every turn, GS has been there with a slightly better seat at the table and better inside information than its competitors. The Treasury Secretary happens to be a former GS CEO. Just an unfortunate coincidence, I’m sure.

As always, in this never-ending looting operation, the rules are bent and modified willy-nilly to support a favored class of institutions and individuals.

We now have an openly two-tiered system.

The FDIC expansion explained

Regarding the expansion of the FDIC powers to include guaranteeing the senior debt of banks and their holding companies…in reviewing the details, I think I figured it out.

Here’s the text:

The Secretary of the Treasury, in consultation with the President and upon the recommendation of the Boards of the FDIC and the Federal Reserve, has invoked the systemic risk exception of the FDIC Improvement Act of 1991. [Edit: love the name]

This action will provide the FDIC with flexibility to provide a 100 percent guarantee for newly-issued senior unsecured debt and non-interest bearing transaction deposit accounts at FDIC insured institutions subject to the terms outlined below.

Scope of Eligible Entities

Eligible institutions would include: 1) FDIC-insured depository institutions, 2) U.S. bank holding companies, 3) U.S. financial holding companies, and 4) U.S. savings and loan holding companies that engage only in activities that are permissible for financial holding companies to conduct under section 4(k) of the Bank Holding Company Act ("Eligible Entities").

Not all companies are eligible, but "bank holding companies" are eligible.

Hmmmm…seems that I recently heard something about somebody switching from being an investment bank to a bank holding company recently…who was that? Oh. Here it is.

On Sept. 21, in a move that fundamentally changed the shape of Wall Street, Goldman and Morgan Stanley, the last major American investment banks, asked the Federal Reserve to change their status to bank holding companies.

Goldman would now look much like a commercial bank, with significantly tighter regulations and much closer supervision by bank examiners from several government agencies.

Yes, I remember being confused by this move at the time as it made no sense. At least the explanations did not smell right. We were told that GS and MS "asked" to be placed under "significantly tighter regulations and much closer supervision by bank examiners from several government agencies."

That would have been a first.

It is now clear to me what happened. The government guarantee of all senior debt was already in the works some time ago, and GS and MS hopped on that gravy train. At every turn, GS has been there with a slightly better seat at the table and better inside information than its competitors. The Treasury Secretary happens to be a former GS CEO. Just an unfortunate coincidence, I’m sure.

As always, in this never-ending looting operation, the rules are bent and modified willy-nilly to support a favored class of institutions and individuals.

We now have an openly two-tiered system.

Total 1968 items

Community

by blaggers

by blaggers

GoldSilver.com

Learn more