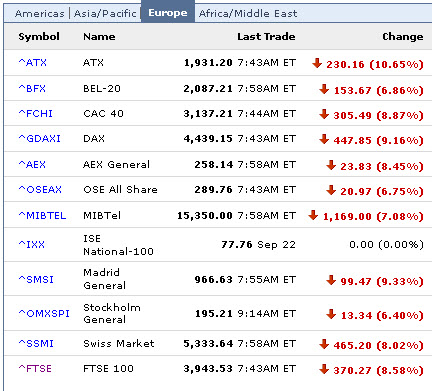

One of the dominant myths of America is that we practice one of the

freest forms of capitalism on the face of the planet. Hard work and

prudence are rewarded, while Schumpeter’s ‘creative destruction’ quickly cleans out the mistakes.

Unlike most myths, this one apparently lacks a kernel of truth at the core.

As the details emerge over the various bailouts and market distortions,

it is becoming clearer that moral hazard has been increased, not

lessened, and that those who behaved prudently during the credit bubble

insanity are going to be punished.

Some are getting angry:

[quote]Community banking executives around the country responded

with anger yesterday to the Bush administration’s strategy of investing

$250 billion in financial firms, saying they don’t need the money,

resent the intrusion and feel it’s unfair to rescue companies from

their own mistakes.

And in offices around the country, bankers simmered.

Peter Fitzgerald, chairman of Chain Bridge Bank in McLean, said he was "much

chagrined that we will be punished for behaving prudently by now having

to face reckless competitors who all of a sudden are subsidized by the

federal government."

At Evergreen Federal Bank in Grants Pass, Ore., chief executive Brady

Adams said he has more than 2,000 loans outstanding and only three

borrowers behind on payments. "We

don’t need a bailout, and if other banks had run their banks like we

ran our bank, they wouldn’t have needed a bailout, either," Adams said. [/quote]

Punishing the Prudent

by Chris Martenson

One of the dominant myths of America is that we practice one of the

freest forms of capitalism on the face of the planet. Hard work and

prudence are rewarded, while Schumpeter’s ‘creative destruction’ quickly cleans out the mistakes.

Unlike most myths, this one apparently lacks a kernel of truth at the core.

As the details emerge over the various bailouts and market distortions,

it is becoming clearer that moral hazard has been increased, not

lessened, and that those who behaved prudently during the credit bubble

insanity are going to be punished.

Some are getting angry:

[quote]Community banking executives around the country responded

with anger yesterday to the Bush administration’s strategy of investing

$250 billion in financial firms, saying they don’t need the money,

resent the intrusion and feel it’s unfair to rescue companies from

their own mistakes.

And in offices around the country, bankers simmered.

Peter Fitzgerald, chairman of Chain Bridge Bank in McLean, said he was "much

chagrined that we will be punished for behaving prudently by now having

to face reckless competitors who all of a sudden are subsidized by the

federal government."

At Evergreen Federal Bank in Grants Pass, Ore., chief executive Brady

Adams said he has more than 2,000 loans outstanding and only three

borrowers behind on payments. "We

don’t need a bailout, and if other banks had run their banks like we

ran our bank, they wouldn’t have needed a bailout, either," Adams said. [/quote]